The Shariah Compliance Bottleneck Nobody Talks About (And How to Fix It)

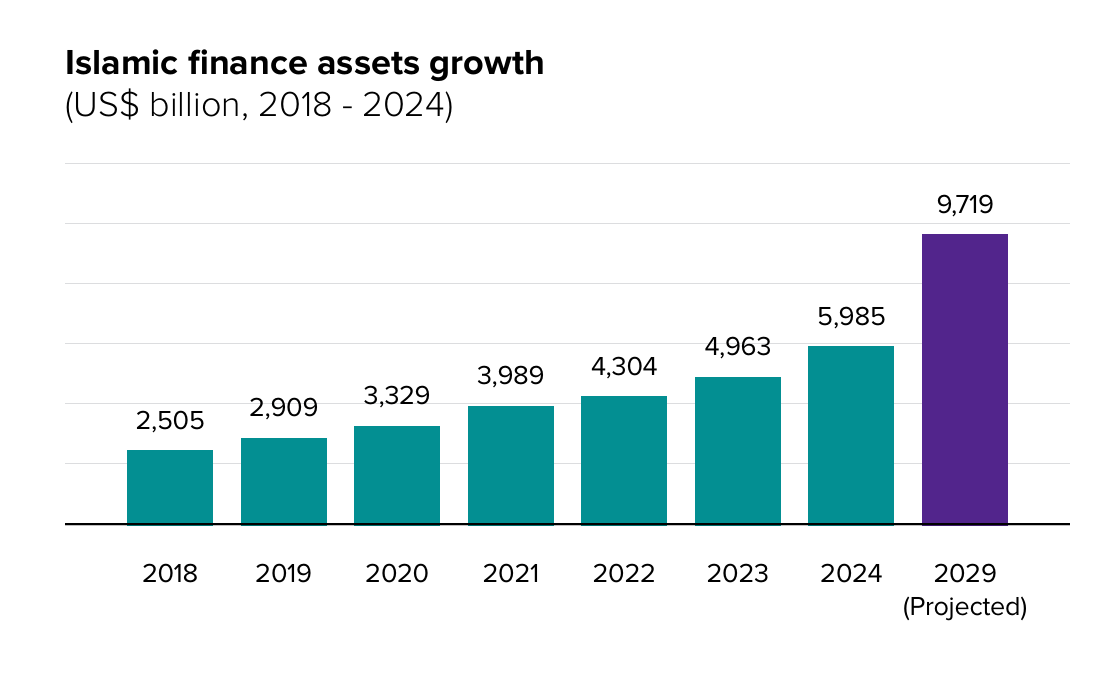

Islamic finance is no longer a niche. Global Islamic finance assets reached $5.98 trillion in 2024, growing 21% year-on-year according to the ICD-LSEG Islamic Finance Development Report 2025, with projections to hit $9.7 trillion by 2029. That is real scale. And with scale comes a problem that the industry has been tiptoeing around for years.

(Image Source - ICD – LSEG Islamic Finance Development Report 2025)

A $6 Trillion Industry Running on a Handful of Experts

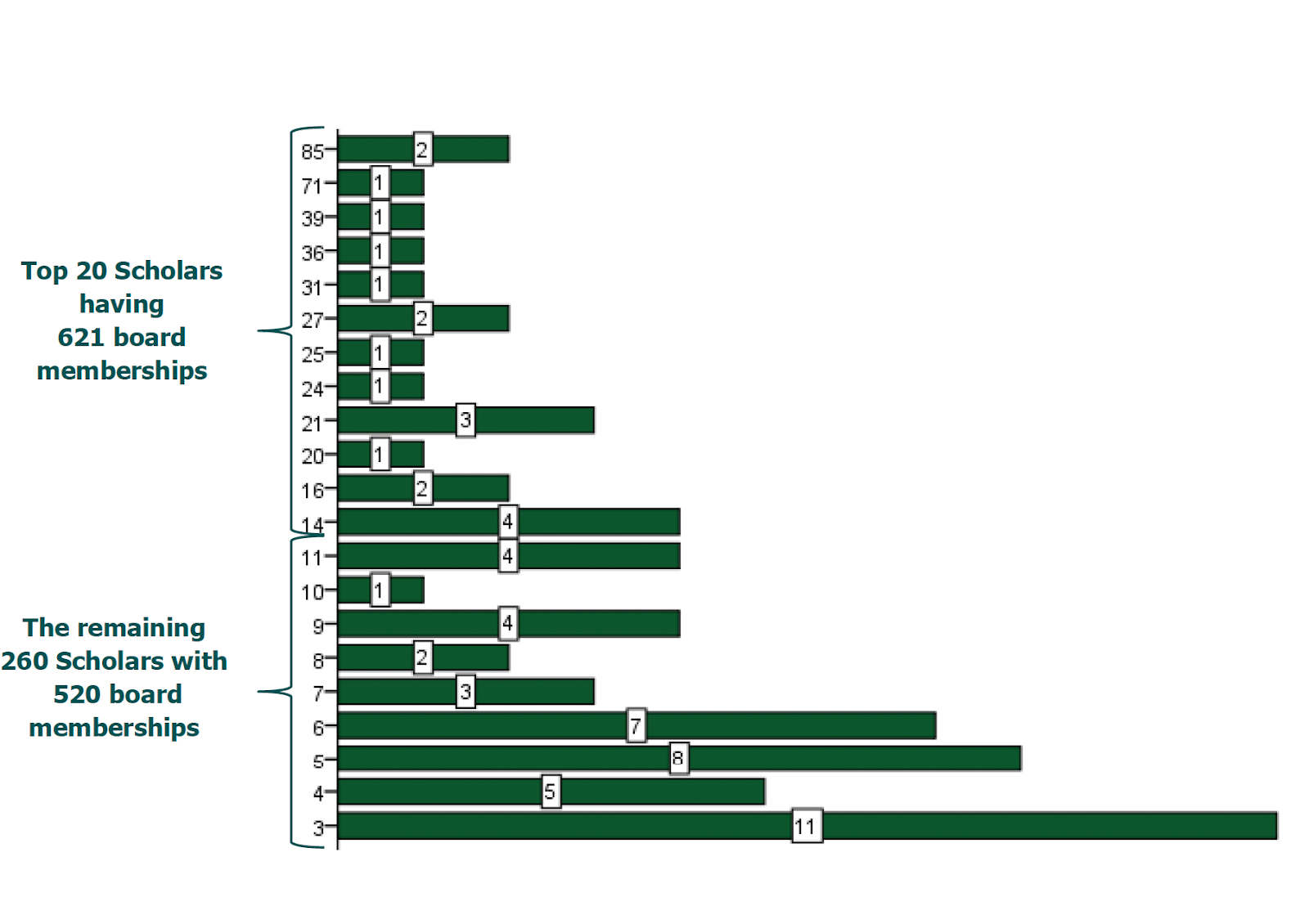

Here is a number that should concern anyone in Islamic finance: a landmark analysis from 2010 using data on Shariah scholars sourced from Zawya, found that the top 20 Shariah scholars held 621 board memberships across more than 370 Islamic financial institutions in 28 countries, while the remaining 260 scholars held 520 positions. This meant that a very small circle of scholars effectively dominated Shariah decision-making across the industry.

(Image Source : The Small World of Islamic Finance ; Shariah Scholars and Governance - A Network Analytic Perspective, Murat Ünal, 19 January 2011; Funds@Work)

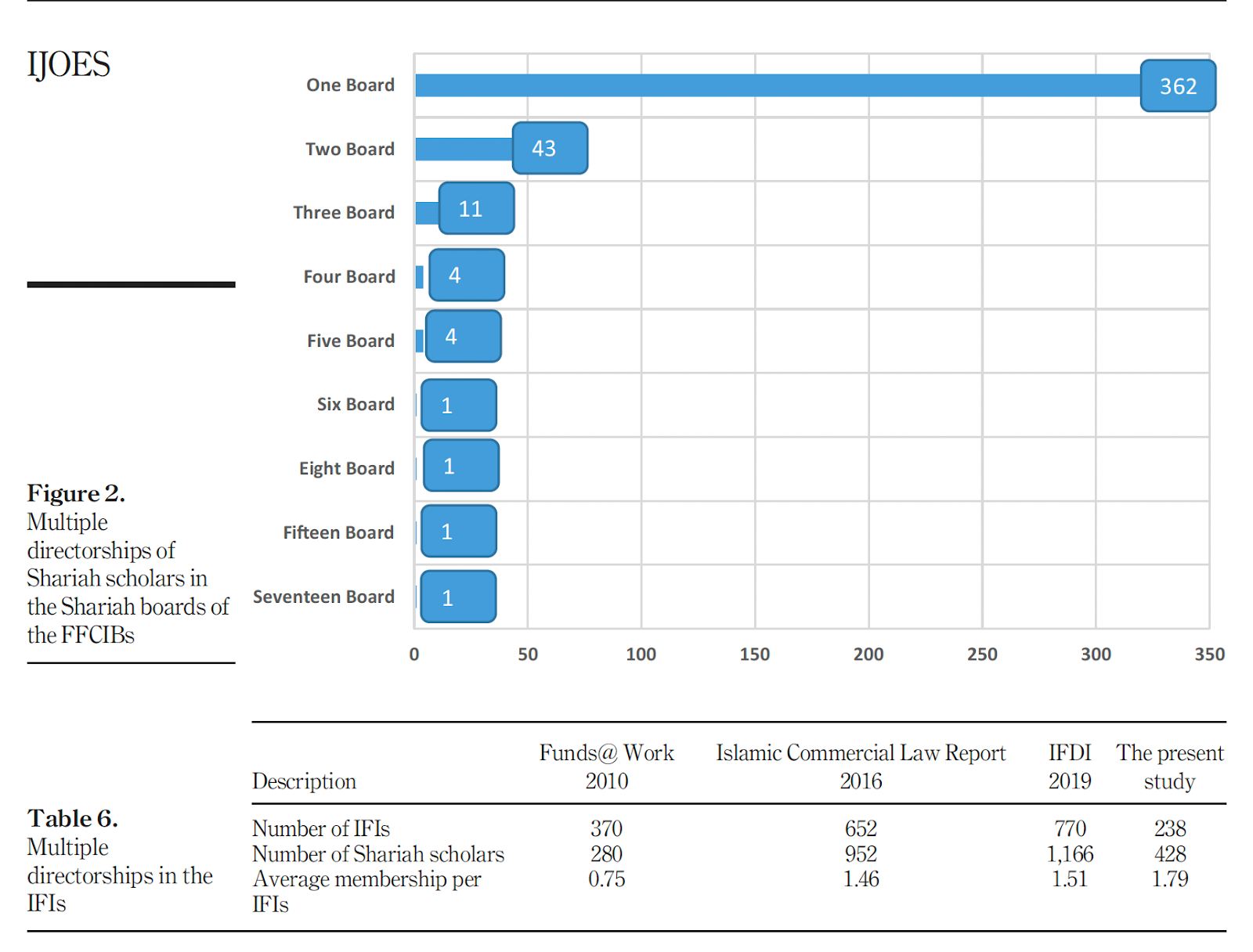

More than a decade later, a global empirical survey of Shariah supervisory boards in 238 full-fledged Islamic commercial banks shows that the pattern of concentration has not gone away. In that 2019 dataset, 428 Shariah scholars occupied 522 board seats, with the top 10 scholars alone holding 74 positions (an average of 7.4 each) and the top 20 holding 106 positions.

Together, these studies show that a handful of individuals still sit at the center of Shariah governance for hundreds of institutions worldwide, even as industry assets have grown into the trillions.

And these scholars are not doing simple work. They are reviewing product structures against AAOIFI’s 59 Shariah standards (part of 117 total standards spanning Shariah, accounting, auditing, ethics, and governance), cross-referencing rulings across four major schools of Islamic jurisprudence (madhahib), checking alignment with local regulatory requirements across jurisdictions like Qatar, UAE, Saudi Arabia, Malaysia, Kuwait, and Bahrain, and mapping every decision back to the higher objectives of Islamic law known as the Maqasid al-Shariah.

That process, for a single product review, can take weeks.

Where the Time Actually Goes

The compliance burden in financial services is well documented. Globally, financial institutions spend an estimated $206 billion per year on financial crime compliance alone. Industry reports also estimate that compliance operating costs have increased by over 60% compared to pre-financial crisis levels.

But Islamic finance adds a unique additional layer. Beyond the standard regulatory requirements that every financial institution faces, Islamic financial institutions must also maintain Shariah governance frameworks, manage fatwa issuance and renewal cycles, conduct annual Shariah audits, handle income purification for any non-compliant revenue, and ensure cross-jurisdictional fatwa harmonization when operating across borders.

Most of this work is still done manually. Scholars spend a disproportionate amount of their time on information gathering rather than on the scholarly reasoning (ijtihad) that only they can provide. They dig through PDFs of AAOIFI standards, cross-reference local regulatory requirements, check scholarly opinions across madhahib, and piece together rulings from institutional memory that often lives in someone’s head rather than in a searchable system.

The knowledge exists. The standards are published. The scholarly opinions are documented. But they sit in silos, scattered across different documents, different languages, and different institutional memories.

The Real Risk: Superficial Shariah Compliance

This bottleneck creates a second problem that is harder to quantify but potentially more damaging: a growing risk of superficial Shariah compliance.

This occurs when products carry a Shariah-compliant label without substantively meeting the principles behind that label. A product might have received a fatwa at launch, but the product structure has since changed. It might reference AAOIFI alignment in its marketing materials, but the actual mechanics have drifted from the original ruling.

Detecting this requires deep expertise. It requires checking whether the fatwa is current, whether it covers the product as structured today, whether compliance with one standard creates conflicts with another, and whether the product serves the higher objectives of Shariah beyond just technical box-checking.

With scholars stretched across 50 or more boards each, the time and attention needed for this level of scrutiny is simply not available at the scale the industry now demands.

What Technology Should (and Should Not) Do

The natural instinct is to say, “AI will solve this.” But the Islamic finance industry has good reason to be cautious about that claim. Shariah rulings require ijtihad, a form of scholarly reasoning that weighs evidence, context, and the higher objectives of Islamic law. That is fundamentally human work, and it should remain human work.

The opportunity is not in replacing scholars. It is in giving them back a significant portion of their time currently consumed by information retrieval, so they can focus on the work that actually requires their judgment.

This is the thinking behind Ask Ali, an AI-powered Shariah compliance tool built by ZeroH. Ali does not issue fatwas or make rulings. What it does is surface the relevant AAOIFI standard for a given question, present scholarly opinions across all four madhahib side by side, map every answer to the five objectives of Maqasid al-Shariah, and show its sources for every single response. No black boxes.

When a compliance officer uploads a product structure, Ali returns a structured analysis with citations, severity ratings, and specific recommendations. Not as a replacement for the Shariah board’s review, but as the preparation that makes that review faster and more thorough.

“When we started building Ask Ali, I assumed the biggest challenge would be the technology. It wasn't. It was discovering that fewer than 20 scholars sit on the boards of hundreds of institutions, and that a single fatwa issued years ago might still be the only thing standing behind a product that's been restructured multiple times since. The real problem that we identified was that knowledge is trapped in documents nobody can find, in languages not everyone reads, across jurisdictions that don't talk to each other. So we built Ask Ali, not to replace the scholars but to fix the plumbing”. — Intesar Haquani, Chief Business Officer, Blade Labs

Why This Matters Now

Two forces are converging that make this moment different from five years ago.

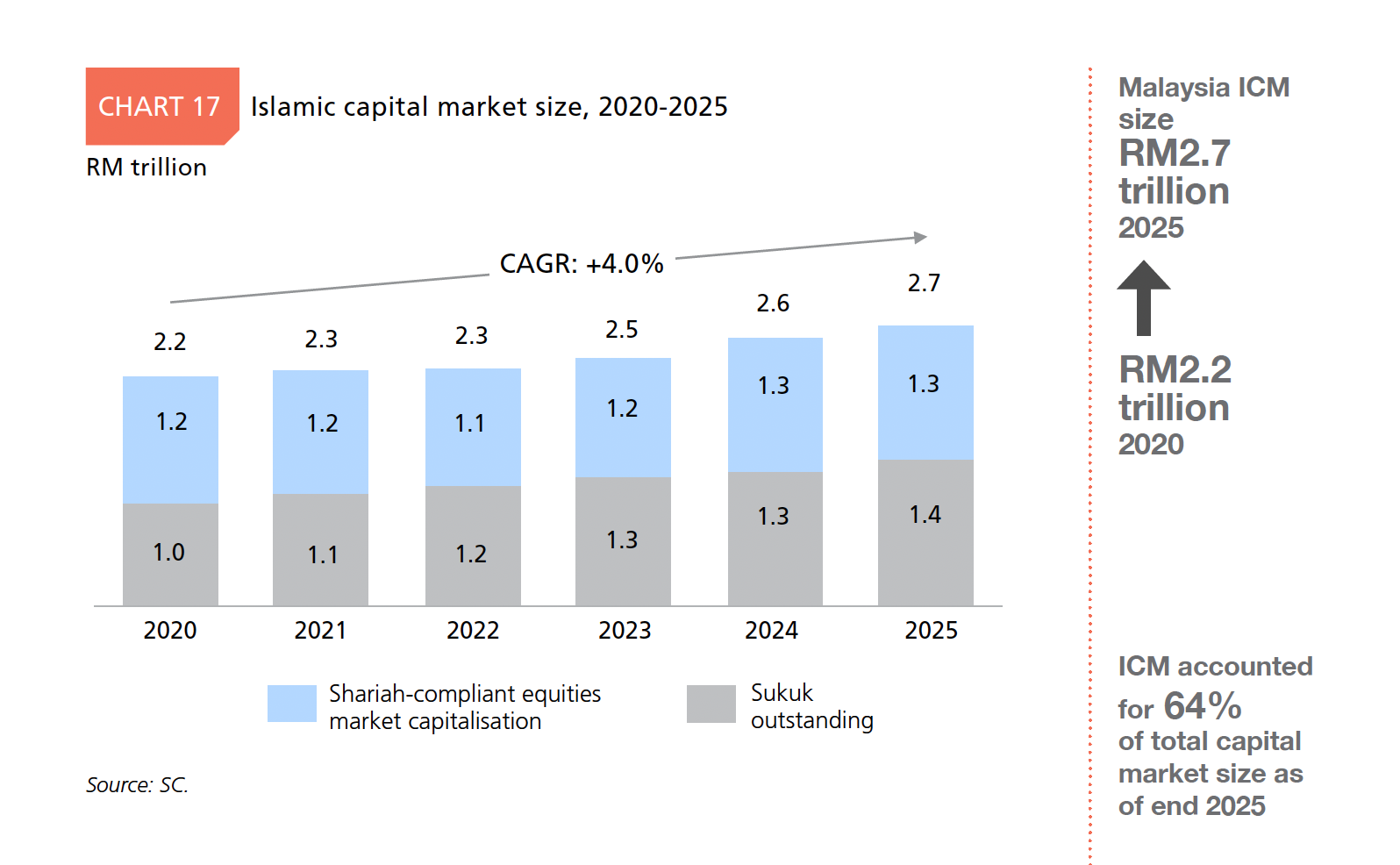

First, regulators are actively calling for it. Malaysia’s Securities Commission published its Capital Market Masterplan 2026-2030, which calls for AI-based digital screening tools for Shariah compliance and ESG alignment across jurisdictions. Malaysia’s Islamic Capital Market stands at approximately RM2.7 trillion, representing 64% of the country’s total capital market of RM4.3 trillion and the largest Islamic capital market in the world. When the regulator of the world's largest Islamic capital market mandates AI-powered Shariah screening, it sets the global standards.

(Image Source - Securities Commission Malaysia, Capital Markets Masterplan 2026-2030)

Second, the next generation of investors demands it. Research consistently shows that a majority of Gen Z and millennial investors in Malaysia prioritize ethical and social alignment in their investments, and a growing share already use AI-driven tools for financial guidance. The expectation of instant, transparent, and traceable compliance is not a future state. It is a current requirement.

The Standard for Compliance AI

The global RegTech market is valued at roughly $19–24 billion in 2025, with double-digit growth projected. But the Islamic finance segment remains underserved. Shariah compliance is still largely manual, fragmented, and without standardized international frameworks.

Ask Ali is built on a simple principle: every answer must trace back to a source. No summaries without citations, no conclusions without the standard or ruling behind them.

What it does is narrow but deep. Upload a Musharakah contract, and Ali walks through it clause by clause against AAOIFI standards, flagging where a loss allocation cap violates SS-12 or where a capital return guarantee quietly transforms the structure into prohibited debt. Ask about Tawarruq, and Ali lays out the Hanafi, Maliki, Shafi'i, and Hanbali positions alongside the OIC Fiqh Academy resolution, with the scholarly evidence and conditions for each. Every product gets scored against the five Maqasid objectives. When a structure invokes Darura (the necessity exception), Ali applies the classical constraints: proportionality, time limits, active development of a compliant alternative, and mandatory Shariah board review.

Every finding traces back to a specific standard, a specific paragraph, a specific scholarly source. Nothing is summarized away. Nothing has to be taken on faith.

The point is not to hand the scholar a conclusion. It is to hand the scholar everything they need to reach one, in minutes instead of weeks. For an industry that grew 21% last year on the shoulders of a few hundred overextended experts, that is not a nice-to-have. That is infrastructure.

Ask Ali is currently in early access. Learn more at https://www.zeroh.io/ask-ali/beta